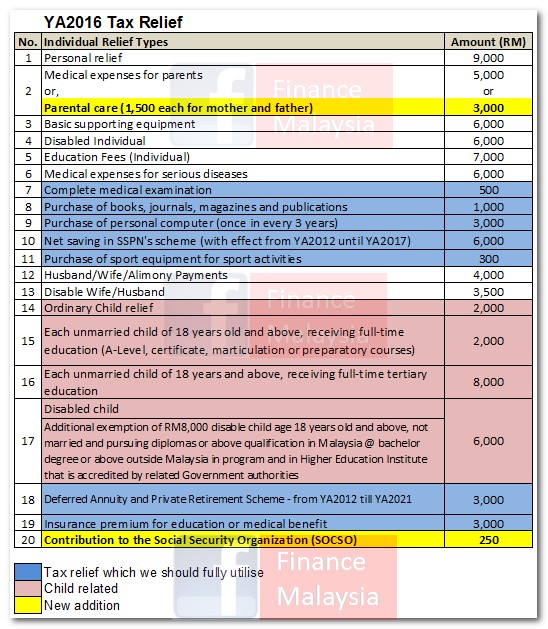

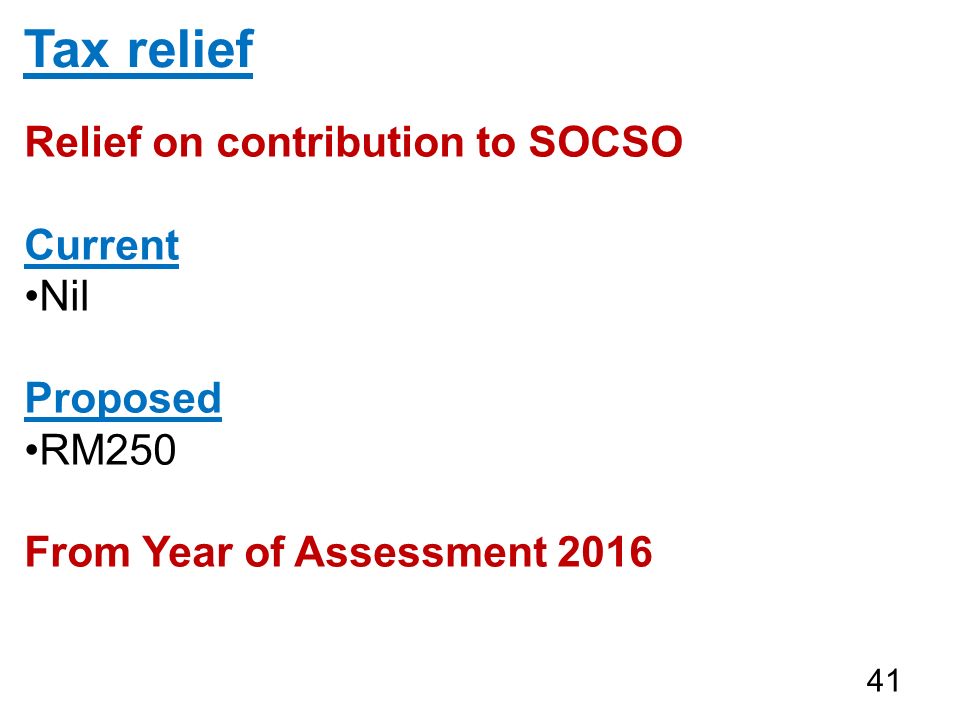

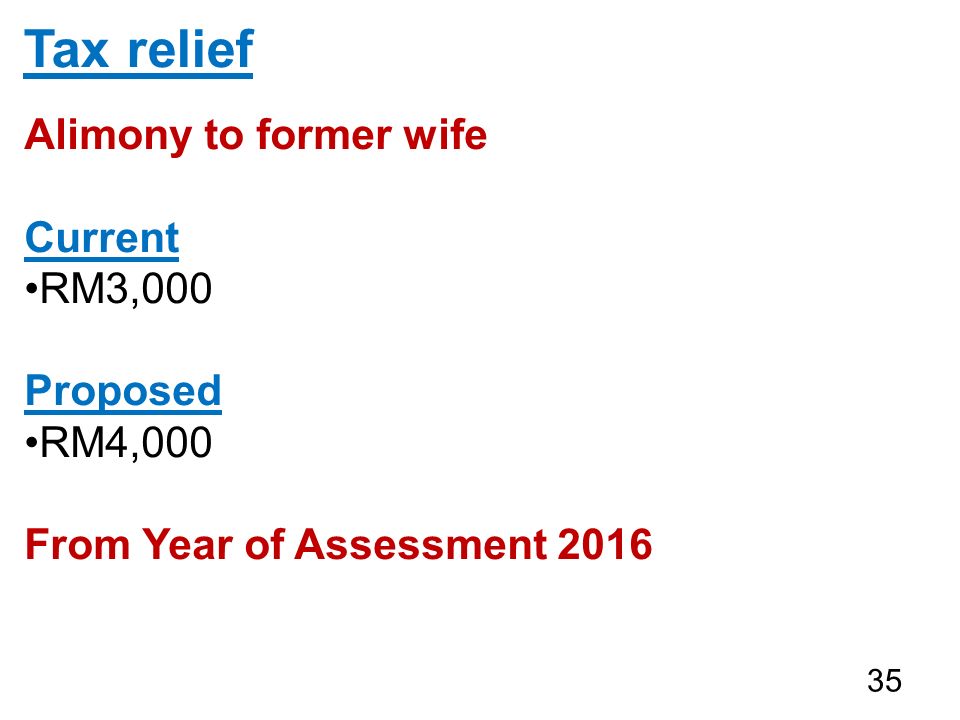

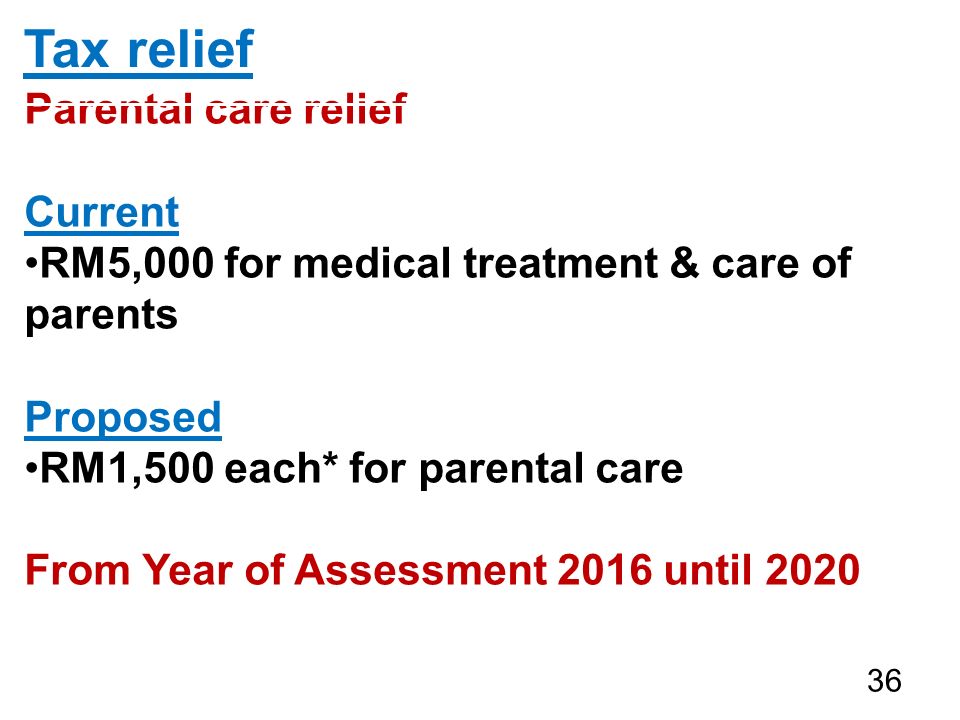

Tax Reliefs For Year Of Assessment 2016

Finance Malaysia Blogspot 2016 Personal Income Tax Relief Figure Out First Before E Filing

The Gobear Complete Guide To Lhdn Income Tax Reliefs Gobear Malaysia

Malaysian Income Tax Relief 2020 For Ya 2019 Tax Filing

How To Save On Income Tax In Singapore Heartland Boy

Budget 2016 Chua Tia Guan Corporate Individual Income Tax Rm M Forecast Companies51 28858 17565 24068 32074 381 Individual22 97723 05524 42328 15530 Ppt Download

Budget 2016 Chua Tia Guan Corporate Individual Income Tax Rm M Forecast Companies51 28858 17565 24068 32074 381 Individual22 97723 05524 42328 15530 Ppt Download

Each year of assessment ya or statutory tax year starts on the first date of the year ie 1 january and ends on 31 december.

Tax reliefs for year of assessment 2016. The tax reduction will only be applicable to the final tax for the year of assessment 2015 16 but not to the provisional tax of the same year. Under the penjana recovery plan there will also be an increase in income tax relief for parents on childcare services expenses from rm2 000 to rm3 000 however this is not applicable when you file this year as it only applies to the year of assessment. The tax system will be more progressive under a new measure that caps the amount of personal income tax relief an individual can claim. This relief is applicable for year assessment 2013 and 2015 only.

The relevant legislation for the tax reduction was passed by the legislative council and. A personal income tax relief cap of 80 000 applies to the total amount of all tax reliefs claimed for each year of assessment. The basis period for a year. The financial secretary proposed a one off reduction of profits tax salaries tax and tax under personal assessment for the year of assessment 2019 20 by 100 subject to a ceiling of 20 000 per case.

The limit will be set at 80 000 from year of assessment. Reducing profits tax salaries tax and tax under personal assessment for the year of assessment 2019 20. Excess balance if any will be refunded. The provisional tax paid will be applied to pay the final tax for the year of assessment 2015 16 and the provisional tax for the year of assessment 2016 17.

Special relief of rm2 000 will be given to tax payers earning on income of up to rm8 000 per month aggregate income of up to rm96 000 annually. You should continue to claim the personal reliefs if you have met the qualifying conditions. The year of assessment is the year of which the income tax is charged after calculation.

Personal Income Tax 2016 Guide Part 4

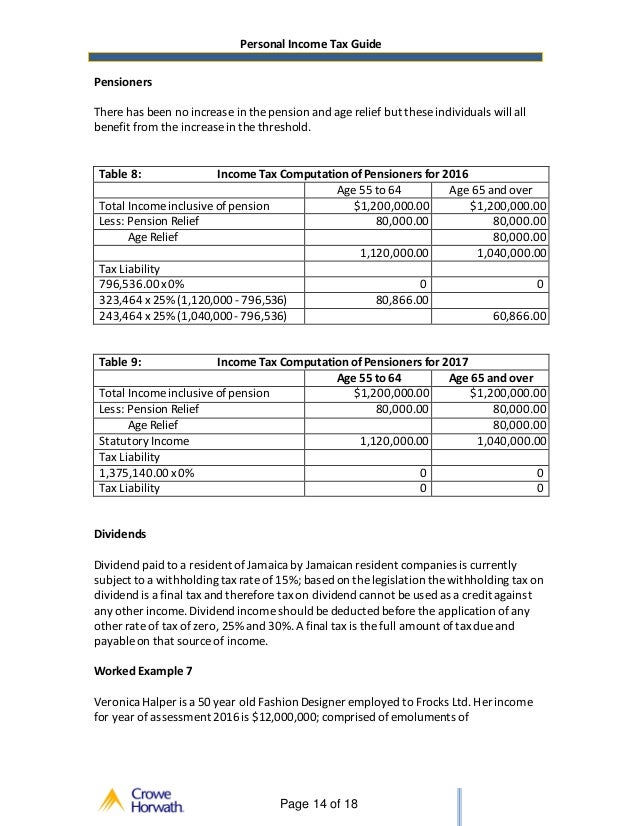

Jamaica Personal Income Tax Guide 2016 Edition 1

The Gobear Complete Guide To Lhdn Income Tax Reliefs Gobear Malaysia

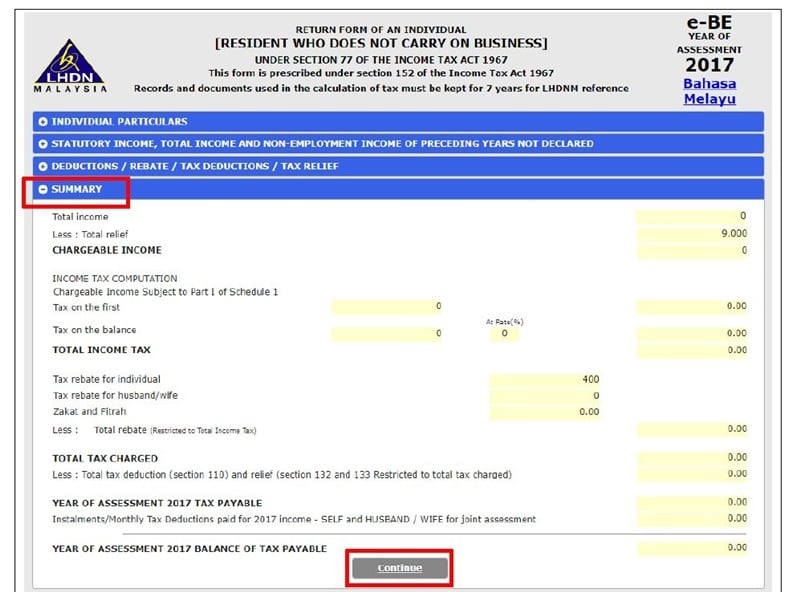

Malaysia Personal Income Tax Guide 2017

Personal Income Tax E Filing For First Timers In Malaysia

Malaysia Personal Income Tax Guide 2017

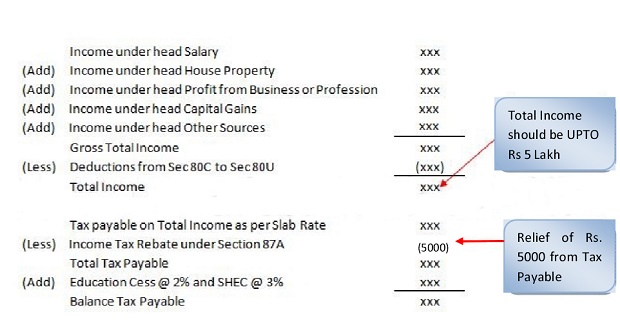

Income Tax Rebate U S 87a For A Y 2017 18 F Y 2016 17

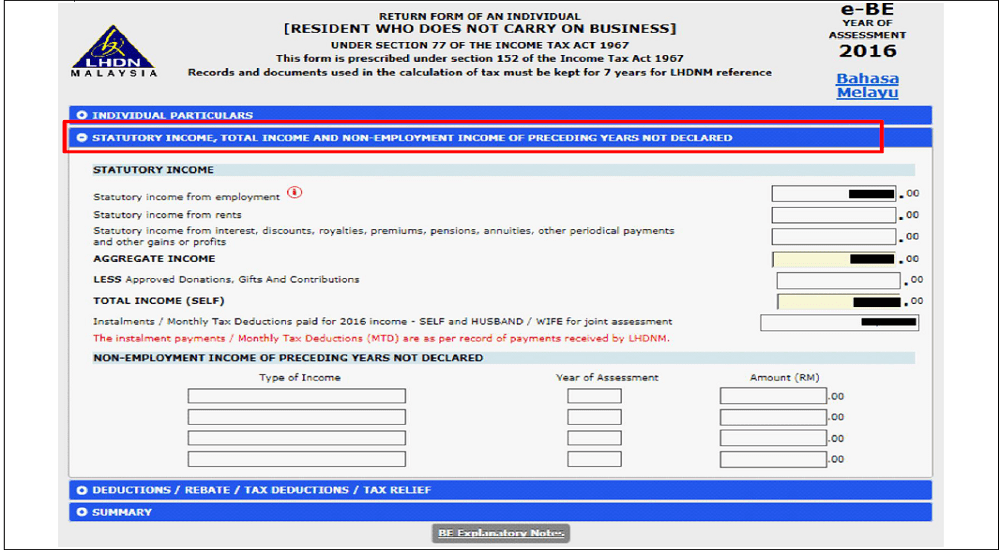

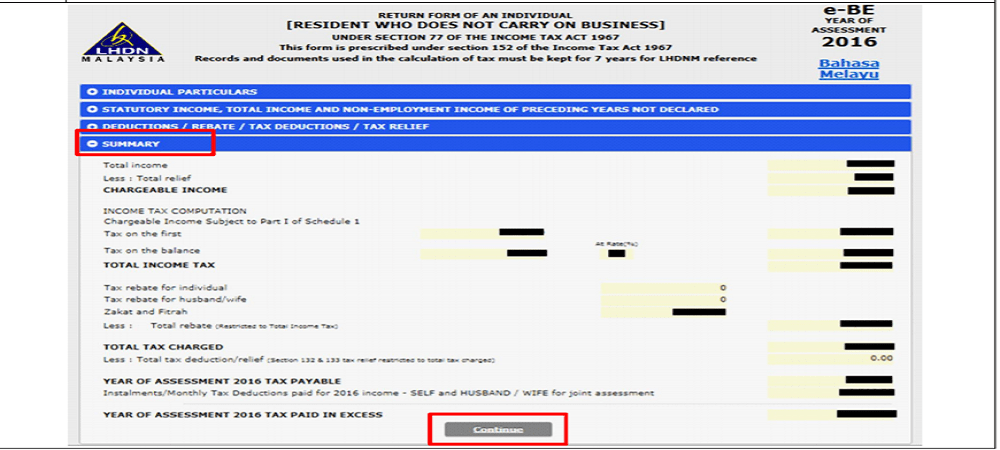

Personal Income Tax E Filing For First Timers In Malaysia Mypf My

Personal Income Tax E Filing For First Timers In Malaysia Mypf My

The Gobear Complete Guide To Lhdn Income Tax Reliefs Gobear Malaysia

The Complete Income Tax Reliefs For Malaysia 2019 Imoney

Malaysia Personal Income Tax Guide 2019 Ya 2018