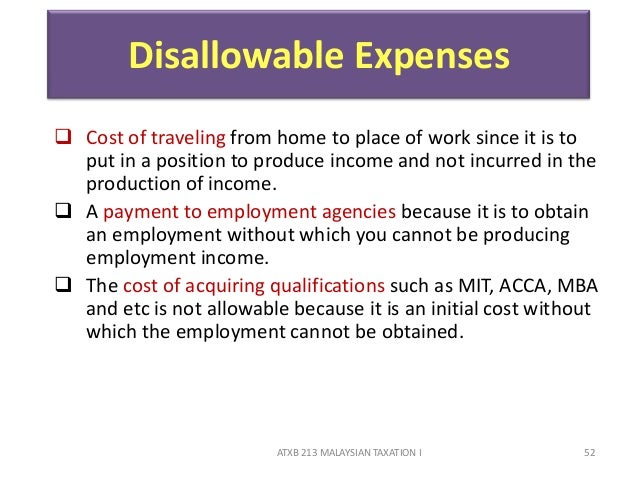

Non Allowable Expenses For Corporation Tax Malaysia

Chapter 5 Corporate Tax Stds 2

Chapter 5 Corporate Tax Stds 2

Chapter 5 Corporate Tax Stds 2

Income Tax Deductions List Fy 2019 Malaysian Income Tax Relief 2020 Tax Filing Guide

Chapter 5 Corporate Tax Stds 2

Chapter 5 Corporate Tax Stds 2

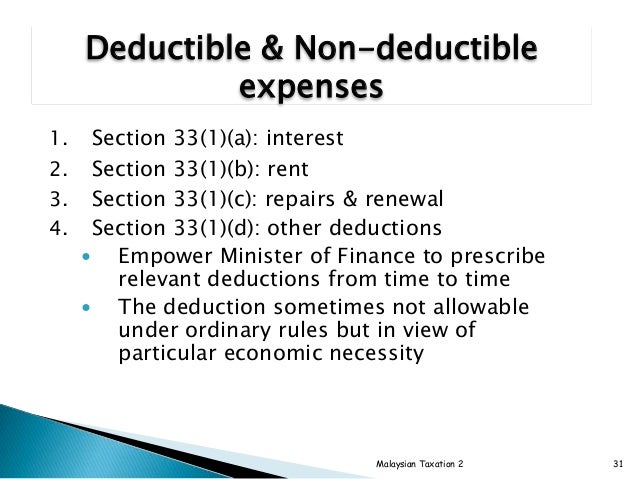

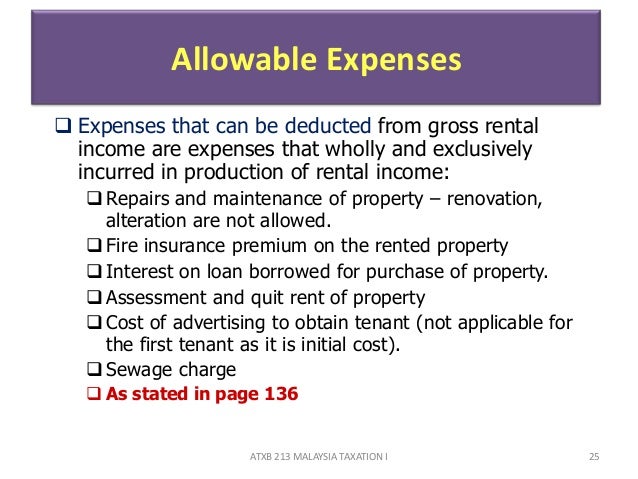

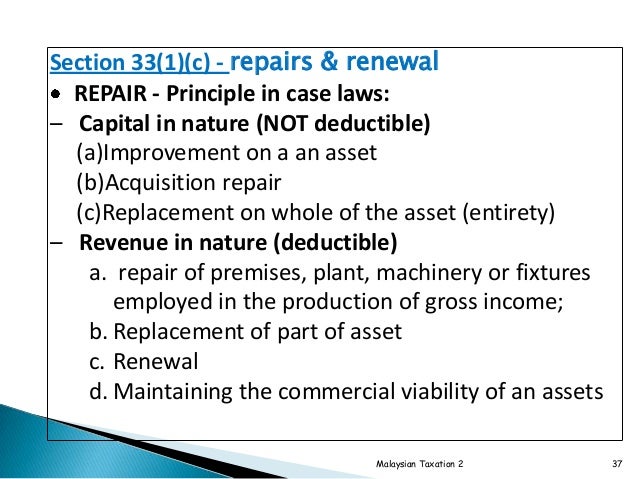

Interest expense is allowed as a deduction if the expense was incurred on any money borrowed and employed in the production of gross income or laid out on assets used or held for the production of gross income.

Non allowable expenses for corporation tax malaysia. Other allowable business expenses. Malaysia offers a wide range of tax incentives for the promotion of investments in. The proportion of interest expense will be allowed against the non business income. Legal and professional fees.

6 3 annual corporate filings and meeting expenses a secretarial fees. For both resident and non resident companies corporate income tax cit is imposed on income accruing in or derived from malaysia. To the special commissioners of income tax and the courts. The following are more common non allowable expenses.

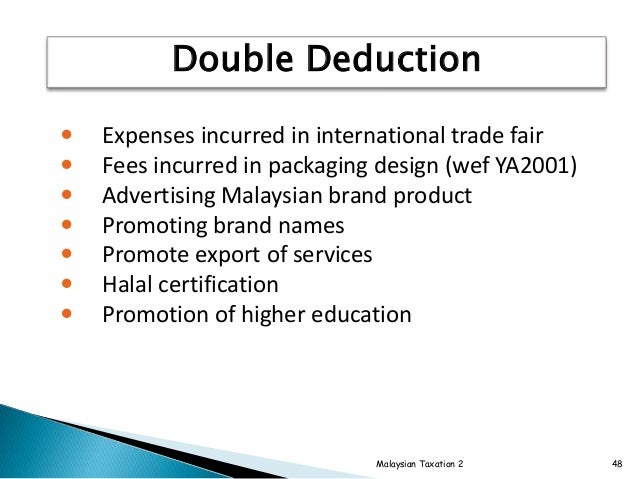

Legal fees are usually allowable and this includes costs of chasing debts defending trademarks preparing legal agreements. Allowable specific expenses double deduction expenses allowable under income tax act 1967. The current cit rates are provided in the following table. Export allowances business expenses.

6 5 legal expense incurred by a landlord. Mosque building fund zakat. 50 allowable tax incentives. Exchange loss arising from transactions that are non trade or capital in nature.

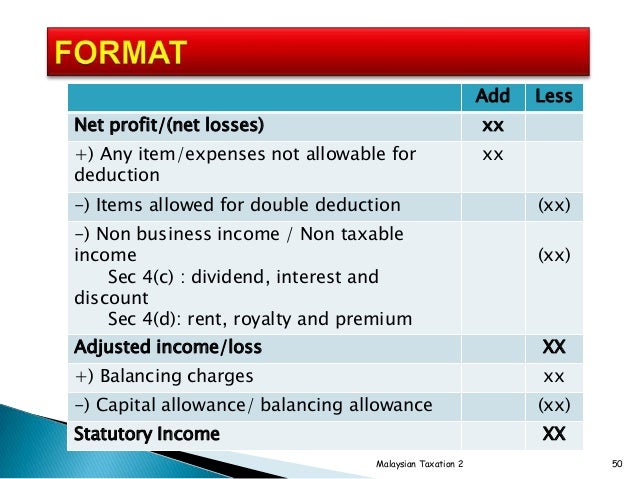

A company or. Adjusted income from business source is derived from gross income after deduction of business expenses such as. B cost of appeal against income tax assessment i e. And if you deduct an expense that doesn t qualify you might be faced with a tax notice or tax audit.

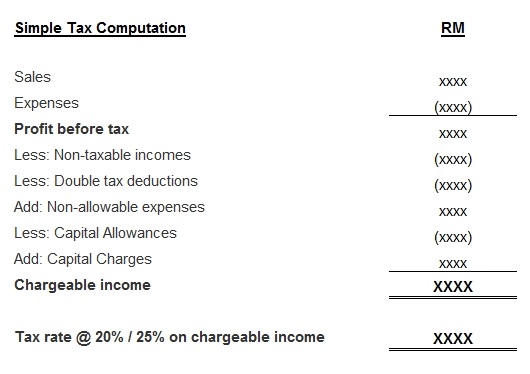

B annual general meeting expenses. Malaysia corporate taxes on corporate income last reviewed 01 july 2020. Expenses that are. 2 tax treatment of business expenses i p 3 tax treatment of business expenses q r 4 tax treatment of business expenses s z for more information on how to make tax adjustments such as adding back non deductible business expenses to arrive at the income that is chargeable to tax please refer to preparing a tax computation.

Staff entertaining is an allowable expense for company tax purposes whereas client entertaining may be an allowable expense and a portion may be disallowed for company tax purposes. It is frequently unclear whether a certain tax expense might qualify as a tax deduction or not. Expenses incurred prior to commencement of business however revenue expenses incurred 1 year before the accounting year in which the company earns its first dollar of business receipt are tax deductible from ya2012 onwards fixed assets written off. 6 4 income tax returns a cost of filing of tax returns and tax computations.

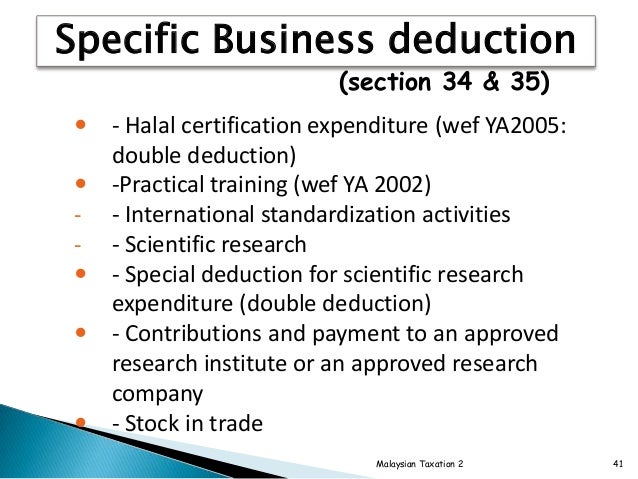

Our malaysia corporate income tax guide. Nondeductible tax deductions expenses. Effective ya 2013 the amount of r r costs that qualify for tax deduction as a business expense is capped at 300 000 for every relevant three year period.

Smeinfo Understanding Tax

Chapter 5 Corporate Tax Stds 2

Corporate Tax Malaysia 2020 For Smes Comprehensive Guide Biztory Cloud Accounting

Chapter 5 Corporate Tax Stds 2

Smeinfo Understanding Tax

Chapter 5 Non Business Income Students

Estimated Chargeable Income A Step By Step Guide To Calculating Eci

Smeinfo Understanding Tax

Chapter 5 Corporate Tax Stds 2

Nbc Group How To Calculate Tax Estimate For Cp204

Smeinfo Understanding Tax

Malaysia Taxation Junior Diary Investment Holding Charge Under 60f 60fa

Ks Chia Tax Accounting Blog How To Maximise Your Entertainment Expenses Deduction